The problems of banks – and I mean the traditional brick and mortar ones – seem endless. Already struggling with rising costs and the competition of FinTech disruptors, they have now come under pressure due to the impact of the Coronavirus pandemic. However, fundamental things have gone wrong for a while at the incumbents. FinTech presents a growing threat, but banks have long got essential aspects wrong and, what is worse, have not learned to respond to the digitalization of the financial industry. A personal example and a fitting case study.

Last week, I received a couple of letters from my local bank. For many people that might already be something odd since they have already moved away from a local bank to a digital competitor or have long gone paperless. Even though I have an online account and do all my transactions from the comfort of my home, going paperless does not seem to be an option.

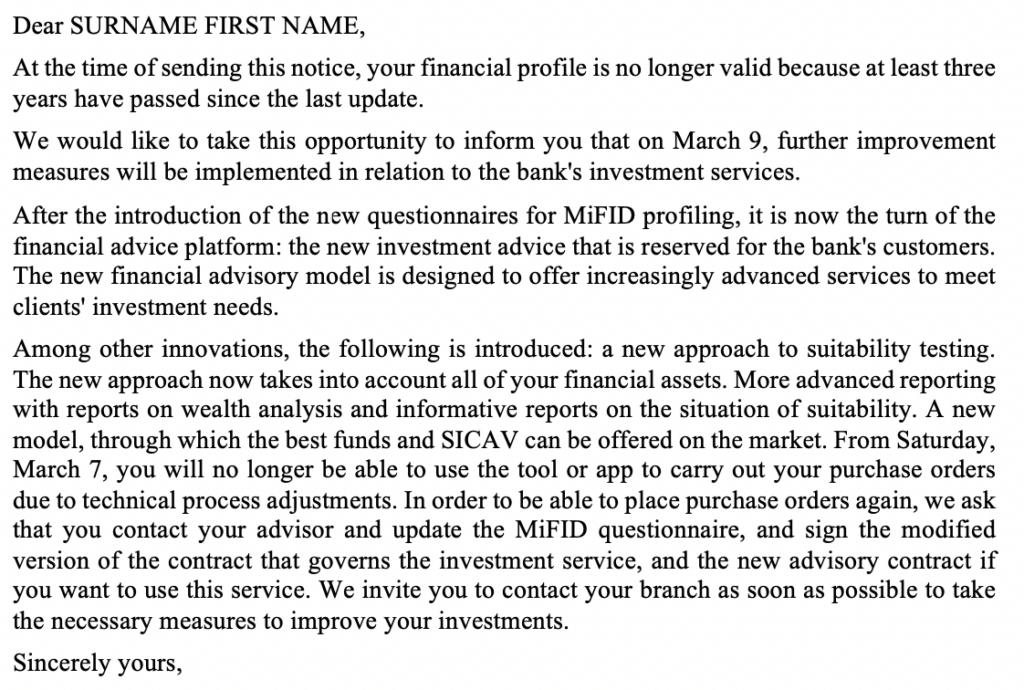

It was about changes to my investment profile as of 31 December 2019, MiFID questionnaires and how I could improve my investments. Here is what it said:

I have reproduced the letter in translated form (it’s clumsier in the original) to highlight a few points in a moment. And to give the full picture, here a few more bits: To begin with, the letter is dated 2 January and names my customer contact as author. It is hard to believe that the letter took more than three months for an inner-city journey. Secondly, it is clearly an automated letter (I know of two other recipients, which have got the same letter, with one of the two only having a company account, thus this particular message was not even relevant as confirmed upon request), so why bother adding my customer contact as the sender? Thirdly, the letter states that if I do not respond by 9 March 2020, I will no longer be able to trade after 7 March. And lastly, of these friendly notifications, I did not get one, but three copies of these friendly notifications. One for me and two for my underage kids.

Now, don’t get me wrong. It certainly isn’t the most serious problem in times when lives across the entire planet are impacted by the Coronavirus pandemic. The existence of individuals and businesses are at stake and financial institutions play an important part in protecting the economic stability.

Yet, it’s another example for what is wrong at traditional institutions and if this crisis is a good time to reflect and reinvent ourselves for the time after the crisis, perhaps this an element banks ought to focus on. Banking will have to become more personal, whether in the human relationship between your local advisor or on the digital level.

Therefore, a letter like the one in question raises a number of concerns:

1) Communication:

Even for someone familiar on a professional level with MiFID 2, much of the requirements and consequences for financial services concerning me personally are sometimes difficult to understand. I believe it is fair to assume that most customers do not have a similar level of regulatory knowledge and will find it even more incomprehensible. I appreciate that the rules introduced by MiFID 2 require the action taken by my bank, i.e. blocking my potential trading activity and notifying me. Yet, I doubt that it’s useful to do it in this particular manner and am sure there could easily be found a better way to communicate and walk me through this process.

2) Customer knowledge:

Now you will say, this all but communication and some do it better than others. True. But what is more concerning is that this letter proves that this bank doesn’t know its clients. Personally, I don’t use any investment services with this bank and have made it quite clear in conversations with advisors, for example, during a meeting that was to update my profile last year. This information, both in terms of interest for financial services offered by the bank as well as the confirmation of my investment profile (i.e. still not interested) do not seem to have found its way into my customer profile. Maybe they just want to use the occasion to give it another shot to sell me investment advisory, maybe it’s only a problem of different systems communicating (or not) with another, but neither installs much faith in the services of my bank. To the point of not knowing its customers, the bank has underlined its ignorance by sending these letters to my underage children who really shouldn’t be targeted for investment advisory services.

3) Trust:

Where to begin? That I receive a letter three month late with a potentially important message (i.e. I couldn’t trade anymore, which would have been quite significant in recent weeks, if I had been an active investor in financial instruments through the bank)? That I receive the notification weeks after the deadline has expired? That the bank does not know what is useful for me or my kids? There are so many red flags that I certainly can’t have much faith in the bank as my trusted financial advisor. This is even more important when the investment services the bank tries to sell me are available elsewhere at a lower cost and in a more convenient way, but that isn’t just a problem of this particular bank but many traditional financial institutions that still haven’t understood how their clients would like to use banking services.

4) Customer service

A standardized letter from my advisor? An unpersonal invitation to show up in the bank to get things going? Is that how the bank thinks it is providing me with a service worth paying for? In a recent survey, 70% of financial institutions named Customer Satisfaction as their top strategic retail banking priorities. Still, digital transformation for many traditional organisations often appears to be limited to Internet banking or the use of .

5) Quality Assessment

Every single communication, every letter, every email or phone call is an example of the quality of service you receive from an organization and its members. This may vary across the different members of staff, but in general you should get a fairly comprehensive idea about the company’s values, strategy and culture.

In this case study, the bank does not properly store and manage important information about its customers like the update to the profile within the last 18 months as opposed to the statement that they had’t spoken to me about it for more than 3 years. The bank claims that the latest update to the profile of my youngest child was more than 3 years ago – a time when the kid wasn’t even born. The notification was apparently sent in January and delivered after the expiry of the deadline. It is a short communication but there are so many things wrong about it. Since this is rather the rule than the exception (I could produce a dozen or more examples that shine an equally unfavourable light), my expectations with regard to the level of service produced by this particular financial institution are rather low and will eventually lead to my moving to another financial institution.

It’s unfortunate though because I honestly believe that customer satisfaction has to be at the centre of any customer relationship but in particular in financial services and the future of finance is combination of digital with a human element to improve the customer experience.

Still, since I frequently interview friends about their experience with other traditional banks, I am under the impression that this is pretty much the norm and that my personal finance future will continue to move towards the digital disruptors. Not only are they cheaper, more efficient and easier to use – while being entirely anonymous, they at least ask relevant questions.