The world has been a rather different place since the global pandemic. Businesses face tighter restrictions and regulations, along with lower profits and increased competition. Financial institutions are often in the thick of this storm, with higher volatility amongst global capital markets.

In 2023, there is greater pressure on financial institutions to use regulatory technology to better govern and report on the data they manage. These regulations are to protect consumers and ensure institutions remain transparent.

Today, we’re discussing the six regulatory challenges every financial institution should know.

What are Regulatory Challenges for Financial Institutions?

Regulations are in place to protect consumers against all manner of risks and protect the stability of the financial industry. In the U.S., regulations are set and monitored by the Federal Reserve, the Securities and Exchange Commission, and the Federal Deposit Insurance Corp. Regulatory challenges refer to the difficulties that institutions might face due to the tighter and changing restrictions set by these bodies.

Key Regulatory Challenges for Financial Institutions

Here are the six main regulatory challenges financial institutions should be aware of to ensure compliance and protect your business.

1) Future-Proofing Fraud Prevention

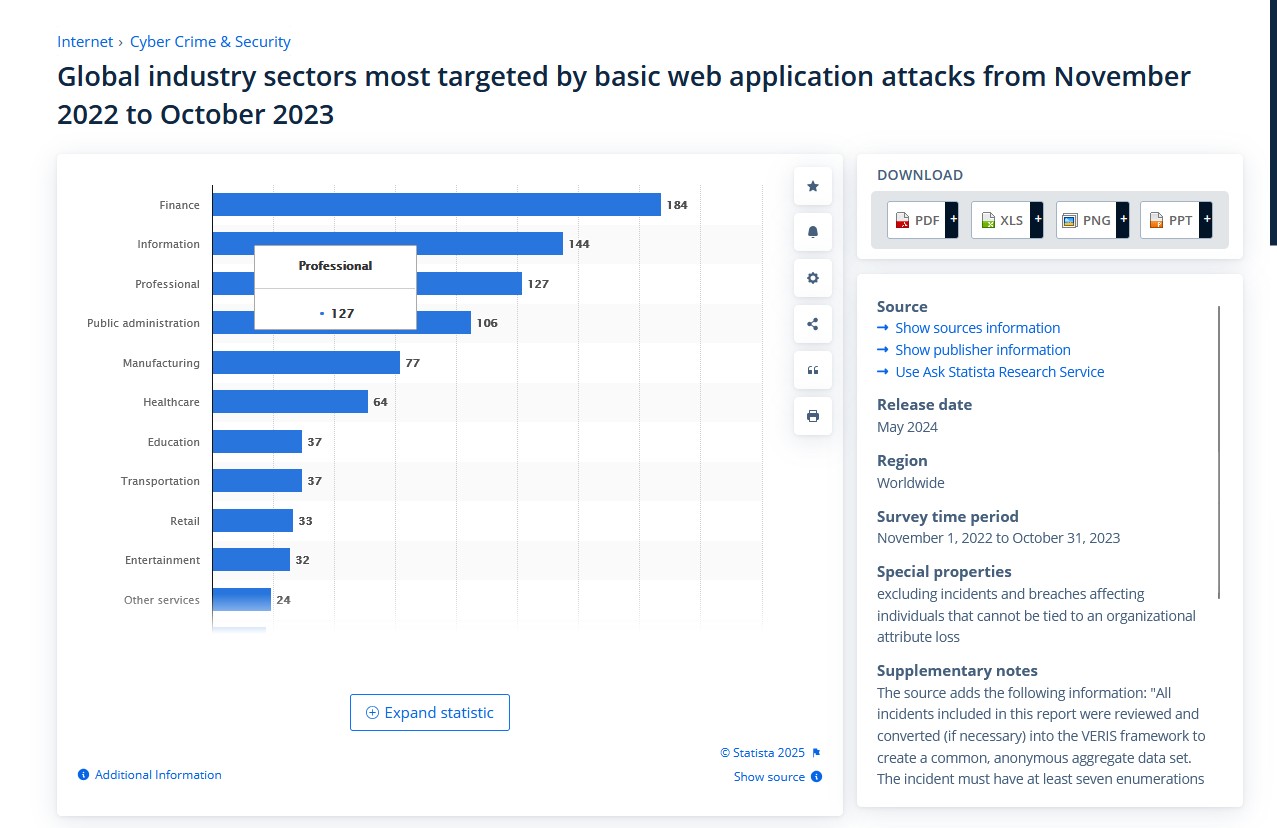

As you’ll see from the graph below, the finance industry is by far the most targeted industry for cyber attacks. Statista states that between 2021 and 2022, there were 173 basic web application attacks throughout the finance industry. The next target industry was information, which saw 121 such attacks, as the graph below illustrates.

Source: Statista

Therefore, financial institutions, in particular, must strive to keep their businesses secure. Institutions need to combine a mix of human and technological data analysis to mitigate risks as best they can. They must have a robust and secure infrastructure and exceptional data security software.

The challenge is that criminals find new and innovative ways to get around such security measures. Therefore, financial institutions need to remain one step ahead by consistently and stringently reviewing and perfecting their fraud prevention measures, such as:

- Conducting regular fraud prevention training.

- Educating your customers on how to protect themselves.

- Implement technologies like biometric authentication, AI-based fraud monitoring systems, and advanced analytics.

- Monitoring transactions in real time.

- Be on alert for internal fraud, both intentional and accidental.

Technologies are the key to meeting fraud prevention regulations. However, employees must be aware of and competent in using these evolving technologies. This, of course, costs time, money, and resources.

Privacy and Data Protection

Fintech companies need to balance compliance with cybersecurity. Customers trust them with sensitive data, like bank account numbers and credit card details. As such, they need to protect it from anyone not authorized to access it to avoid data breaches.

When you use technology to store and manage your customers’ data, you run the risk of someone hacking your systems. You must also consider internal threats of staff accidentally deleting or sharing data with unauthorized people. Therefore, proper training should always take priority.

Here are some steps you can take to ensure your financial institution remains data protection-compliant:

- Back up your data automatically and regularly.

- Restrict access to data so that only the necessary people can view or handle it.

- Encrypt data authentication hardware and specialist software.

- Store devices that contain data in safe places that the company can lock securely.

- Use tools like firewalls, VPNs, and two-factor authentication.

Combining these data protection methods will help you overcome the privacy and data protection challenges you face as a financial institution.

Risk Control

Risk control is not all about cyber security. It’s also about mitigating financial risks associated with investments, for example. Financial institutions must communicate any risks associated with their products and services to protect consumers’ financial interests.

Another area of risk management in the financial industry is ensuring proper affordability assessments of people who apply for credit. They need to carefully balance their risk control procedures with their ability to remain competitive within the market.

You can manage risks effectively by:

- Automating the risk management process to save both time and money.

- Identify risks associated with your company, such as poor credit assessments leading to inappropriate lending.

- Install secure business VoIP phone systems to communicate with customers over the phone.

- Monitor, test, and report on risks, potential risks, and mitigation processes so you can continuously improve.

Adapting to Changing Regulations

Senior management is now being held more accountable for data breaches and lapses in security. The cyber attack boom has made this difficult, and institutions face consequences like larger fines and increased third-party liability. Naturally, this bumps up the cost of insurance, too.

Financial institutions must regularly review their systems and processes to overcome this challenge. They must keep up-to-date with emerging trends. For example, AI is a double-edged sword. While financial institutions can take advantage of it to tighten their security systems and procedures, cybercriminals could also adopt AI technology to bypass these systems.

Understanding the trends and taking a proactive approach can help you adapt to changing regulations efficiently. Part of this is also implementing new processes, strategies, and technologies without adding new risks to your business.

Anti-Money Laundering Schemes

Regulatory bodies are pushing financial institutions to invest more money into systems to fight money laundering. Naturally, financial institutions are a prime target for money laundering schemes.

In 2021, an interagency statement recognized the challenges of implementing anti-money laundering systems. While it may be time to embrace AI, the report states that AI and transaction monitoring tools can cause complexities within model validation. However, there are some practical steps you can take to improve your anti-money laundering schemes:

- Collect customer information, such as job titles and annual income.

- Monitor customer transactions and screen them for suspicious activity.

- Hold deposits made into accounts for at least five days.

- Report suspicious activity to the appropriate authorities.

By integrating robust financial planning and analysis strategies within your anti-money laundering efforts, institutions can ensure that resources efficiently tackle this challenge while adapting to changing financial crime patterns. These analytical insights help optimize compliance procedures and enhance detection mechanisms.

Working From Home

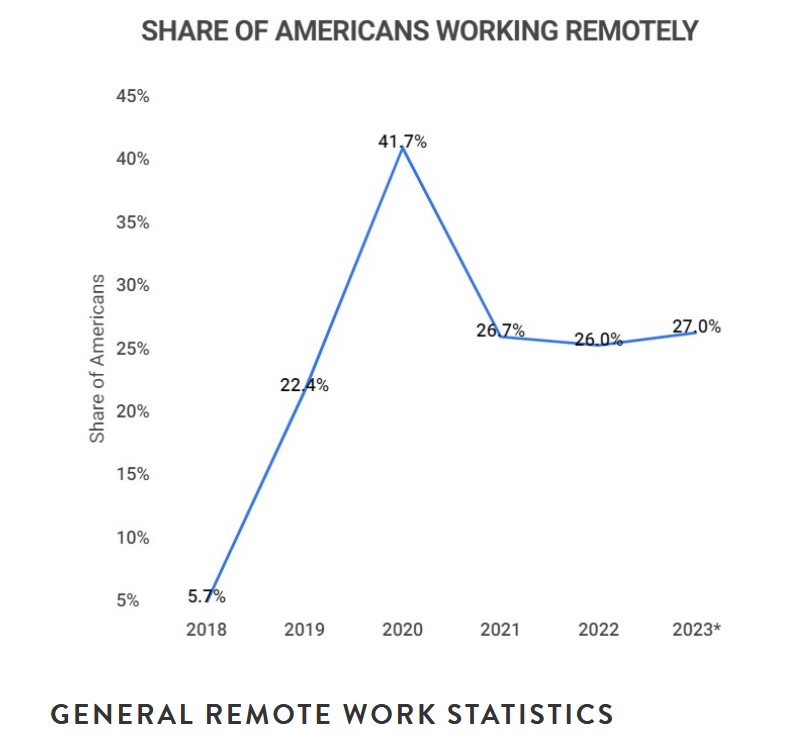

Zippia claims that 23% of U.S. workers work remotely, and 15% of job opportunities are entirely remote. Furthermore, this trend is set to continue.

Source: Zippa

But what does this mean for financial institutions with strict regulatory requirements? After all, you have less control over who sees customer data, and all employees connect to different WiFi. The risks inevitably increase when you have a remote workforce.

Here are some things you can do to combat this challenge:

- Train your employees on cyber security.

- Ensure all employees have cybersecurity software installed on their devices.

- Require employees to use VPNs.

- Set out clear security policies, such as creating strong passwords.

- Use a cloud-hosted PBX for telephone calls.

- Use end-to-end encryption for using chat, emails, and applications.

In addition, considering the sensitivity of financial data and the need for secure collaboration, financial institutions might explore using Virtual Data Rooms (VDRs) for sharing and managing documents securely during remote work. Virtual Data Rooms provide a secure online environment where sensitive documents can be stored, shared, and accessed by authorized personnel while maintaining strict control over access rights and permissions.

Conclusion

With new technologies and trends come new regulatory challenges for financial institutions. Use this article as a guide to help you overcome each challenge.

One of the main themes running through this article is the increased use of technology. Although it might pose some challenges, technology is one of the best lines of defense against attacks. You can incorporate it into your business to help you remain secure and compliant.